Sector Looks Subdued Right after Combined Lender Results, Biden Stimulus Announcement

Essential Takeaways:

- JPM

JPM Morgan beats on leading, bottom traces but warns of financial uncertainty

- Wells Fargo

WFC , Citigroup

C report revenues that miss out on anticipations

- Biden’s stimulus bundle features increasing minimal wage to $15 for each hour

There’s a phrase on Wall Street that buyers normally “buy the rumor and provide the simple fact.”

We may perhaps be viewing some of that this morning just after President-elect Joe Biden late Thursday unveiled a $1.9 trillion stimulus strategy that contains immediate payments, increased extra federal unemployment assistance, state and community federal government assist, and increasing the federal least wage to $15 an hour.

The marketplace has been in an uptrend in section on anticipations of new stimulus from the Biden administration. With that priced in, investors may perhaps be having the true announcement as a time to book some gains. There could also be some worry about how elevating the minimum amount wage could impact companies at a vulnerable time whilst the pandemic carries on.

Biden’s announcement arrived in advance of major bank earnings this morning, which buyers appear to be paying out shut notice to as a opportunity gauge for how the rest of the fourth quarter reporting season may go.

Big Banks Ring the Opening Bell on Earnings Time

The acquire-the-rumor-offer-the-point dynamic may perhaps apply to JPMorgan Chase (JPM) as properly. JPM experienced a large quarter, with income topping expectations and earnings coming in at $3.79 for each share when analysts had envisioned just $2.62. The strong quarter arrived as the financial institution was equipped to unwind some of its loan decline provisions and buying and selling was sturdy amid the help the current market has been seeing from the Federal Reserve.

But JPM shares have been buying and selling 1% decreased in the premarket, potentially a result of JPM possessing been on really a tear, increasing approximately 48% considering that the begin of November.

JPM CEO Jamie Dimon may have contributed to this morning’s standard weak spot, saying there is still “significant in the vicinity of-term financial uncertainty.”

However, whilst the bank is maintaining credit score reserves of far more than $30 billion, the truth that it was able to launch some of the income it experienced established aside for mortgage losses appears good news for the broader overall economy as it proceeds to get well, and as it looks forward to much more stimulus and wider-distribute vaccines.

Turning to the other big financial institution earnings news from this early morning, Wells Fargo’s (WFC) success were combined, with the lender beating anticipations on its bottom line number but lacking on revenue. Legacy issues continued to haunt it, and its CEO mentioned its “results ongoing to be impacted by the unprecedented working setting.” Its shares were off 1.3% in pre-market place investing.

In the meantime, Citigroup’s (C) shares were being also decreased irrespective of an earnings conquer. The financial institution documented a little reduced-than-anticipated revenue.

Very last quarter, the banking companies boosted sector sentiment pertaining to how traders and traders felt about the forthcoming earnings year. This time about, it appears like the response isn’t as optimistic. However, we have not still viewed all the outcomes from the big banking companies.

An upsurge in cash markets trading activity and a extremely robust initial community supplying (IPO) marketplace could bode very well for Q3 outperformers Goldman Sachs

Jobless Claims Uptick, but Reassurance from the Fed

The main a few U.S. indices ended up comparatively muted yesterday as information about President-elect Joe Biden’s stimulus plan came in, new information confirmed the jobs market place has taken a change for the worse, and Federal Reserve Chairman Jerome Powell reiterated what buyers predicted to listen to about fascination premiums and bond buys.

Powell sent on what most in the industry in all probability expected to hear—that the central bank isn’t planning to raise fascination premiums or taper its bond buys any time shortly. Despite individuals resources being in use since of the adverse consequences from the coronavirus on the financial state, Powell also explained the financial state may well be ready to get back again to pre-pandemic levels sooner than feared.

Yet, matters really don’t glimpse notably good appropriate now on the economic front. Knowledge yesterday confirmed that weekly jobless statements rose to their optimum stage because August, spiking to 965,000 when a Briefing.com consensus had been expecting 780,00.

Still, the market opened in positive territory, perhaps as some traders and traders figured the labor sector situation might give lawmakers added incentive to go even more stimulus. As the pandemic has dragged on, it is also possible that Wall Street has grow to be a bit numb to the jobless numbers. It may well be easy to overlook that, even if the determine experienced occur in at 780,000, as expected, that is nevertheless an astronomical quantity compared to exactly where we ended up in advance of the pandemic.

Photographs in the Arm: Stimulus and Vaccines

Stimulus anticipations appeared to buoy the market, just before it ran out of steam towards the close of the session, on hopes that the stimulus actions will help tide the economic system over until eventually vaccines can be widely administered and enable the economy get back again on its ft.

Talking of vaccines, Johnson & Johnson

It would seem that the sector has loads to be optimistic about in spite of the ongoing pandemic. That might be why huge tech-related providers had a down working day. All the FAANG stocks finished the working day decreased, supporting pull down the broader current market. These stocks have been in weighty demand through the pandemic as their size, cash and technology-targeted firms produced them a safe and sound haven investment decision of kinds even though many other businesses experienced a rougher time.

Now, as the vaccine rollouts, stimulus initiatives, and Fed backstopping assistance buyers and traders come to be more optimistic, the huge tech-associated names have been providing way to stocks that stand to advantage when the financial state gets back again to usual. That dynamic was borne out yesterday as the Russell 2000 (RUT)— which is built up of small cap domestic shares that are predicted to do better as the financial restoration continues—managed to raise its gains during the working day, rising much more than 2%, even as the 3 primary U.S. indices pared their gains and ended up in detrimental territory.

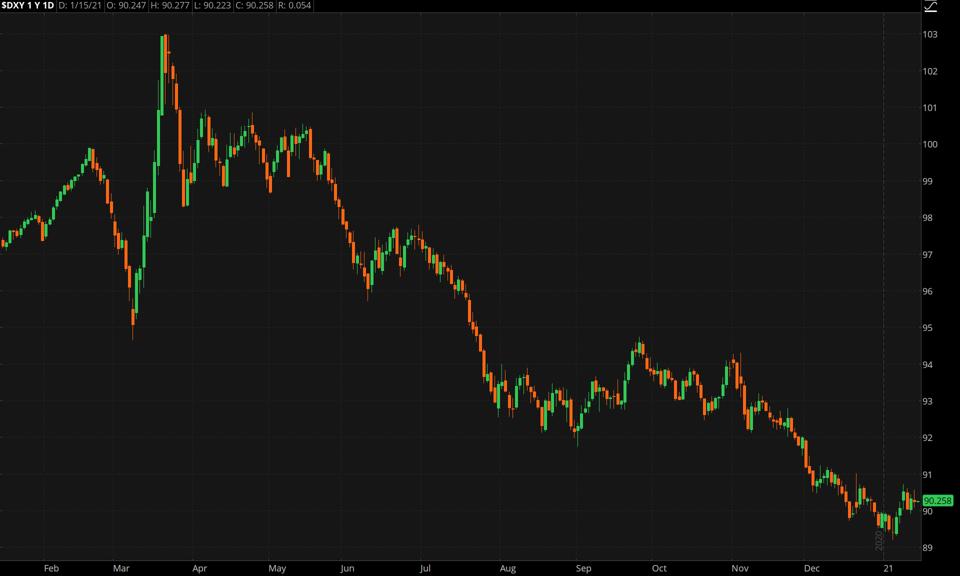

CHART OF THE Day: The ICE U.S. Dollar Index ($DXY), which steps the buck in opposition to a basket of … [+]

Mark Your Calendar: Up coming week’s economic calendar is relatively light, but that doesn’t suggest traders get a total crack from the circulation of critical info. The weekly first jobless claims report may well bear even far more scrutiny on Thursday, as investors check out to discern no matter whether unemployment promises in the 900,000 assortment could possibly come to be a trend for a even though just after this week’s figure. Industry individuals will also get to appear a tiny further into the point out of the housing market with reports on housing commences, constructing permits, and present household gross sales. It could be interesting to see how small mortgage costs are impacting those people quantities. Notable earnings experiences future week incorporate Lender of The united states (BAC), Goldman Sachs (GS), and Netflix

Earnings Outlook A lot less Bad: Speaking of earnings, fourth quarter S&P 500 Index (SPX

Far more (Or Considerably less) Bang For Your Buck: U.S. shares have been in a standard uptrend as buyers have been hopeful that much more stimulus from Congress can enable jumpstart investing on Principal Street. Meanwhile, the Fed’s effortless financial coverage has served boost equities by reducing corporate borrowing expenses and reducing bonds’ attractiveness when compared to stocks. But Wall Street could also be cheering the income “printing” from the Fed and the unparalleled shelling out from Congress due to the fact individuals attempts have been weakening the U.S. greenback. A weaker buck can enhance the gains of multinational organizations by producing their products and solutions fewer pricey in markets overseas. If Apple

TD Ameritrade® commentary for academic uses only. Member SIPC.